Should I Purchase Earthquake Insurance?

Oregon is the third likeliest state to suffer a severe earthquake….

…yet only one in five Oregonians has earthquake insurance. In the interest of protecting your largest asset at the cost of a few hundred dollars per year, we recommend considering this important protection. This is especially relevant in light of all therecent seismic activityin California, Hawaii, and along the Pacific coastline.

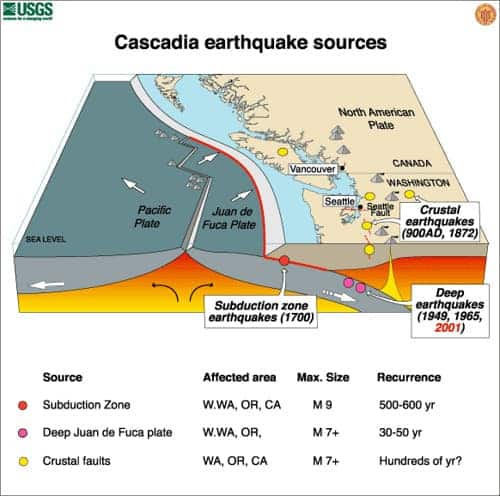

The Cascadia Subduction Zone and the power of the ‘Big One’

Via: Columbia University

Along the entire coast of Oregon runs a fault line called the Cascadia Subduction Zone. This is a planetary feature created when one tectonic plate (in this case the oceanic Juan de Fuca plate) is sliding underneath (subducting) another (the North American continental plate). As Juan De Fuca slides down, the North American plate bunches up with the friction. When enough pressure is built up, the plate flops back down (see image, left), and a very dramatic flop it will be.

For example, the Fukushima quake in 2011 was a 9.1 subduction quake. That quake caused a tsunami with 30-foot waves, completely leveled 120,000 buildings and partially destroyed 726,000 buildings. The economic cost was upwards of $235 billion. The loss of life was over 20,000 and some people are still working to rebuild their homes.

When asked about the destruction estimates for a Cascadia subduction quake ina New Yorker article, Kenneth Murphy of FEMAresponded that the operating “assumption is that everything west of I-5 will be toast.” Pretty straightforward.

We heart Oregon though, and we’re not going anywhere.

However, considering that the odds of a powerful quake happening off the coast in the next 50 years are one in three, it’s best to be prepared.

Earthquake insurance explained

Your insurance agent will have the most precise details, but generally there are three basic components to earthquake insurance coverage.

- Property damage – Most plans cover direct physical loss to property resulting from an earthquake. You’ll pay a deductible, for example, a homeowner with $300,000 in dwelling coverage and a 10% deductible would pay $30,000 before insurance kicks in.

- Personal property coverage – A separate deductible is generally used to cover personal property in your dwelling. This is set by determining a set dollar amount for the contents of your home.

- Loss of rents coverage – If you rent a property, you can insure loss of rent from damaged buildings and inability to find tenants after a quake.

Check with your agent to identify items that cannot be covered or do not need to be covered by earthquake insurance. For example, you’re likely already insured against fire damage through your homeowners policy. Likewise, earthquake insurance typically doesn’t cover damage to landscaping, pools, fences, masonry, storage sheds, automobiles, etc.

How your home affects your coverage

Wooden homes are generally cheaper to insure than brick homes. This is because they are able to flex more with the shaking earth. Several other factors will affect the cost of insurance as well.

- The age of your home (homes built before 1940 tick up in cost).

- Taller homes are more expensive.

- Raised homes are generally cheaper than slab foundation homes.

- If your home is built on sandy soil instead of clay or bedrock, it will have higher premiums.

Saving money on earthquake premiums

Retrofitting your home with various earthquake proofing can help lower your costs. Some examples include:

- Bolting your home to its foundation.

- Bracing the chimney and water heater.

- Installing automatic gas shut-off valves.

- Using plywood to strengthen cripple walls.

- Tying the roof to the studs during roof replacement and tying the roof structure to the wall structure.

Consulting with an expert: Larry Thompson, American Family Insurance

For an experienced perspective, we reached out to Larry Thompson, an agent with American Family insurance for over 20 years, and asked him what kinds of questions he gets most often.

Deductible structures are key. Larry noted that it’s important to make clear that unlike most insurance, earthquake deductibles are a percentage of your coverage. You’ll also pay a separate deductible for personal property inside your home (sofa, TV, etc.). This deductible will also be a percentage of your coverage.

- $500,000 home at 10% = $50,000 deductible.

- $200,000 personal property damage coverage at 10% = $20,000 deductible.

Get educated. Larry’s main emphasis on the topic is to consult your agent and ask questions. Some agencies don’t sell earthquake insurance or might have capped their earthquake policies. Many condo associations include earthquake insurance as most condo HOA boards err on the side of caution. Certain homeowners insurance plans include earthquake coverage as an optional endorsement.

Earthquake insurance rates will rise. As scientific tools become more precise, increasing knowledge about the scope of damage, premiums will rise. The longer our region goes without an earthquake, the more rates will tick up as well.

There are so many variables, and the best way to decide if coverage is right for you is to talk to an expert.

Resources for disaster preparedness for your home and family

Earthquake safety at home – FEMA has created this handy site dedicated to preparing your home and family for an earthquake.

Ready Northwest – A Beaverton-based company, Ready Northwest creates ready-made disaster kits (including an earthquake emergency kit) and provides disaster preparedness consulting for businesses.

Oregon.gov– Oregon’s bureau of emergency management site has several resources, including a handy sheet ofinsurance tipsand an earthquake preparednessguide.

Maps – Should an earthquake occur,this map shows rendezvous points for emergency assistance.

If you have additional questions about earthquake insurance or preparedness, we’re happy to discuss or point you in the right direction. Though the timeline is contested, the Big One is coming one day, and we want to help you take measures now to secure peace of mind over your investments and your family.